Home > News > Industry News

Senior Consultant Xu Feng

On February 9th, Dongfeng Motor and Changan Automobile simultaneously announced that their controlling shareholders are planning a reorganization. If Dongfeng and Changan could merge, the largest automotive group in China and the fifth largest automaker in the world would be born.

Almost simultaneously, on the evening of February 10th, BYD Auto released the "Tian Shen Eye" intelligent driving system with great significance and announced that it would be fully equipped on all models priced at over 100,000 yuan, officially ushering in a new era of intelligent driving for all.

Not long after the Spring Festival of 2025 ended, the automotive industry has already begun to get restless...

01 Current Situation of the New energy Vehicle Industry

Due to the influence of the macroeconomy, the global automotive market has remained sluggish

The automotive industry is a strategic pillar industry for the development of the national economy and an important indicator of a country's industrialization level. It is characterized by being capital-intensive, technology-intensive, and talent-intensive. Moreover, it has a long industrial chain, obvious industrial driving benefits, and broad market prospects. However, affected by the macroeconomy, the current global automotive market is developing relatively sluggishness.

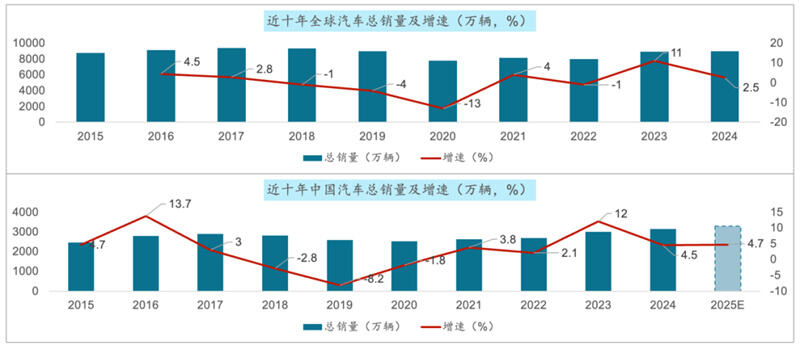

From 2015 to 2024, the total global sales of automobiles increased from only 87.56 million to 89.8 million, with a cumulative growth of 2.6% and a compound annual growth rate of 0.3% over the decade. During the same period, the total sales volume of automobiles in the Chinese market increased from 24.6 million to 31.436 million, with a cumulative growth of 27% and a compound annual growth rate of 2.8% over the past ten years.

2. The sales of passenger vehicles in China's auto market continued to grow, while the overall sales of commercial vehicles declined

In terms of passenger vehicles: 2020 was the year with the lowest sales of passenger vehicles in China in the past decade, reaching 20.18 million units. In the following five years, sales continued to grow. By 2024, the sales of passenger vehicles in China reached 27.56 million units.

In terms of commercial vehicles: Affected by the macroeconomy, China's commercial vehicle market has remained sluggish, falling short of expectations. Over the past decade, it has shown a trend of rising first and then falling. 2020 was the year with the highest sales volume of commercial vehicles in China, reaching 5.13 million units. In the following five years, sales continued to decline. By 2024, the sales volume of commercial vehicles in China was 3.873 million units, falling short of the expected 4 million units.

3. Overseas sales have performed outstandingly, increasing nearly fivefold in the past five years

In terms of domestic sales: It has been moving forward slowly amid fluctuations, generally showing a low-level slow growth trend. From 2015 to 2024, China's domestic auto sales increased from 23.87 million units to 25.58 million units, with a cumulative growth rate of 7%, and a compound annual growth rate of 0.8% over the ten years.

In terms of exports: Over the past decade, China's auto exports have generally shown a rapid development trend. Particularly in the last five years, the volume of China's auto exports has increased nearly fivefold, rising from 994,900 units in 2020 to 5.859 million units in 2024, with a compound annual growth rate of 55.8% over the five years and 26% over the ten years.

4. With the continuous advancement of technologies such as electrification, intelligence and connectivity, new energy vehicles have witnessed explosive growth

Global market: From 2015 to 2024, the global sales of new energy vehicles increased from 643,000 units to 1,823 units in 2024. 60,000 units, an increase of nearly 27 times, with a compound annual growth rate of 45%.

In the Chinese market, over the past decade, the sales of new energy vehicles in China have grown from 331,000 units to 12.866 million units in 2024, an increase of nearly 38 times, with a compound annual growth rate of 50%.

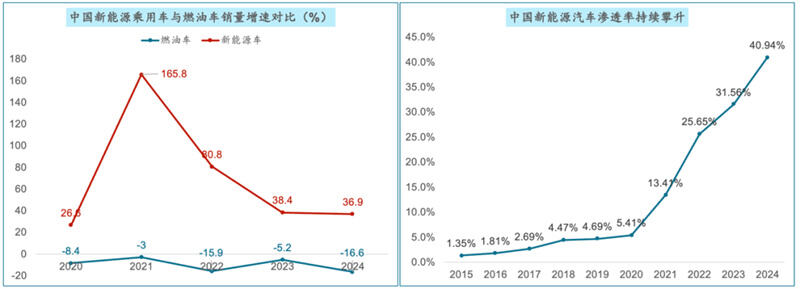

5. In the passenger car market, the fuel vehicle market has continued to decline, while the penetration rate of new energy vehicles has risen rapidly

In the past five years, the sales of new energy vehicles and fuel vehicles in China's passenger car sector have been in stark contrast. The average annual growth rate of new energy vehicles has been 70% over the past five years, while the average annual decline in sales of traditional fuel vehicles has been 9.8%.

The penetration rate of new energy vehicles in China has risen from 1.35% in 2015 to 40.94% in 2024, an increase of over 39 percentage points. It is expected that by 2025, the penetration rate of new energy vehicles in China will exceed 50%.

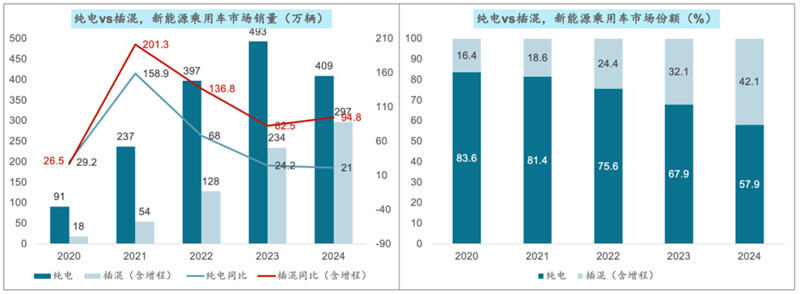

6. The growth rate of pure electric models has weakened, while the share of plug-in hybrid and extended-range models has continued to increase

From the perspective of development trends, as plug-in hybrid/extended-range models can significantly alleviate consumers' range anxiety, offer a more flexible driving experience, and also benefit from advancements in battery technology and cost reductions, they have a more competitive edge over pure electric models, especially in the mid-to-low price range. This makes plug-in hybrid/extended-range models the first choice for consumers to "enter" the new energy vehicle market. The sales volume this year still maintains a high growth rate.

At present, pure electric models still hold the major share, while the market share of plug-in hybrid and extended-range models has increased to 40%.

7. The new energy vehicle industry is currently in a stage of intense competition, with market concentration constantly increasing

At present, China's new energy vehicles are in a stage of extremely fierce competition. New ENERGY VEHICLE consumption is booming, competition has ALSO BECOME extremely cruel, dozens of AUTOMAKERS have been eliminated in the "blood sea", the number of layoffs has reached up to 100,000, more than 400 enterprises have disappeared in the past six years....

In 2024, the market concentration of the top three new energy vehicle sales in China reached 51.4%, an increase of 11.4 percentage points compared with the previous year. The market concentration of the top5 reached 65.2, an increase of 3 percentage points compared to the previous year. In the current competitive landscape, which is increasingly favorable for leading automakers, the market concentration is also continuously rising. Meanwhile, the market concentration of the top10 reached 85.5%, a decrease of 1.4 percentage points compared to 2023. Compared with the top5, These mid-tier automakers are under greater competitive pressure.

02 Future Development Characteristics of the New energy Vehicle Industry

The market continues to grow and the penetration rate keeps rising. According to IDC's forecast, the market size of new energy passenger vehicles in China will exceed 23 million units by 2028, with a compound annual growth rate of 22.8%. It is expected that the market penetration rate of new energy passenger vehicles will exceed 50% by 2025, reaching 56%.

2. Technology is constantly innovating and its application is becoming more extensive. The energy density of batteries is constantly increasing, the cost is gradually decreasing, and the lifespan is prolonged. New breakthroughs have been made in the research and development of all-solid-state batteries, which will further enhance the performance and safety of new energy vehicles. The functions of autonomous driving are constantly upgrading, and the perception, analysis, decision-making and execution capabilities of vehicles are gradually improving, moving towards a higher level of autonomous driving. With the large-scale implementation of urban NOA, high-speed NOA and high-end intelligent driving are expected to become standard features for products priced between 100,000 and 200,000 yuan and those priced over 200,000 yuan respectively.

3. The upgrading of industries has accelerated, and the clustering of industries has become more obvious. The product upgrade of new energy passenger vehicles is accelerating. Various automakers are constantly launching new models, and the product iteration speed has been shortened to about half a year to meet consumers' constantly changing demands for new energy vehicles and enhance market competitiveness. The trend of clustering in the new energy vehicle industry is becoming increasingly prominent. For instance, Anhui Province has established an integrated development pattern featuring the dual-core linkage of Hefei and Wuhu. Shenzhen has a dense distribution of upstream and downstream enterprises in the intelligent connected vehicle industry chain. Chongqing is striving to build a trillion-yuan intelligent connected new energy vehicle industry cluster.

4. Intensified market competition and the rise of new brands. Traditional automakers such as BYD, Geely, and Changan have all made significant investments and performed well in the new energy sector, with their market shares continuously expanding. Meanwhile, new force brands like NIO, XPeng, and Li Auto have stood out in the mid-to-high-end market, driving the rapid development of the new energy vehicle market. Additionally, players like HarmonyOS and Xiaomi have risen rapidly, intensifying market competition.

5. Diverse consumer demands, with an increase in high-end demands. The sales of high-end cars with a price exceeding 300,000 yuan have grown rapidly. Consumers have put forward higher requirements for the appearance, interior and configuration of passenger cars, driving various car brands to constantly innovate and launch models and configurations that better meet consumers' expectations.

6. With intensified policy support, future growth is promising. The government's supportive policies for the new energy vehicle industry will continue to drive market growth, including subsidies, tax reduction and exemption for purchase, and the construction of charging piles.

7. Exports have grown rapidly and international influence has increased. The international influence of Chinese auto brands is on the rise, and the export market will become an important growth point for the passenger car industry.

8. Insufficient utilization of production capacity still poses challenges. Some automakers have insufficient capacity utilization and are at risk of being shut down, merged or restructured. Inventory pressure is also relatively high during specific periods, and automakers need to reasonably control their production pace and inventory levels. The export market is confronted with risks such as international trade frictions and tariff barriers. It is necessary to pay attention to changes in the international trade situation and policies, and adjust export strategies and market layouts in a timely manner.

Three major development trends of the New energy vehicle Market in 2025

The economic foundation that supported the explosive growth of the automotive industry no longer exists. Slow growth and long-term competition are the main themes of the auto market. Automakers should be prepared for a "long-term battle".

Slow growth and long-term competition are the main themes of the auto market

2. The first-time purchase demand has been restricted and declined. Revitalizing the existing demand has become a new engine for market growth. Under the policy stimulus, the short-term sales volume still rose steadily.

By 2025, the penetration rate of new energy vehicles will remain above 50%. PHEV remains the biggest driver of growth, with its incremental contribution expected to exceed 60%.

Under the background of competition for existing market share, the overall profitability of the industry is under pressure. Accelerating the construction of brand moats, building core competitiveness, and seizing users' minds are the keys to winning the market.

5. The trend of consumption upgrade continues, and market demand is shifting towards the price range of 150,000 to 250,000 yuan (with both price and experience upgrades) and personalized models (upgrading without raising the price).

6. High-end self-driving is about to cross the innovation gap and gradually penetrate into mass consumption. In the second half, the optimization of smart electric technology experience and cost will become the key to competition.

Hot News

Hot News2025-04-22

2025-04-12

2025-04-15

2025-04-22